Numismatist. 54 year member ANA. Former ANA Senior Authenticator. Winner of four ANA Heath Literary Awards; three Wayte and Olga Raymond Literary Awards; Numismatist of the Year Award 2009, and ANA Lifetime Achievement Award 2020. Author of "The Enigmatic Lincoln Cents of 1922," Available now from Whitman or Amazon.

@jmski52 said: The reason metals are moving isnt because of the financial system...but other things, bigger things, are breaking down.

Such as.....?

There's more than one reason (including a breakdown of the fiat money financial system), and the bigger things >you mentioned include global competition for resources....In addition to that, the debt-based monetary system, >institutionalized by Western bankers has been the undoing of the West.

Maybe in the 1970's for a few years, when currencies went from fixed to floating and inflation roared.

Your statement about "Western bankers" is patently untrue since governments have been the instigators, even subtly coercing "Western bankers" into buying government debt (i.e., Europe).

@coastaljerseyguy said:

Why would you say that, are you a trader? Since most futures contracts close out for cash and not physical >delivery, I would think short traders do care when spot is higher then future months contracts.

My experience in the few times I stopped by the metals trading desk -- I spent much more time at the bond desk -- is that contango was a real headwing for futures trading given the negative carry. This problem was exaccerbated with leverage which many hedge funds and institutions utilized.

@Goldminers said:

Platinum was back up strong to $2,370 as I am writing. Checked with APMEX what they pay for graded proof >platinum eagles 69 or 70 and was offered $2155 or $215 under spot just now. Their lowest selling price is >$2,755 or $385 above spot for a spread of $600 per ounce!

Never understood these wide-spreads when the price rises or volumes pick up. That's a really wide spread when it should have narrowed, IMO.

@Goldminers said:

Platinum was back up strong to $2,370 as I am writing. Checked with APMEX what they pay for graded proof >platinum eagles 69 or 70 and was offered $2155 or $215 under spot just now. Their lowest selling price is >$2,755 or $385 above spot for a spread of $600 per ounce!

Never understood these wide-spreads when the price rises or volumes pick up. That's a really wide spread when it should have narrowed, IMO.

Platinum has always had pretty wide spreads. It's a low volume metal. I'm guessing most dealers have to pay less and charge more because there really isn't a ton of retail demand. It's even worse for metals like Rhodium.

@batumi said:

Word is Powell is saying diving boards will be installed on the top floor of his bloated white elephant project.

The architecture of the Mariner Eccles Building is very ornate and requires specialized labor and materials. The cost overruns even BEFORE Covid were going to be there.

Since the Fed is the 1 institution in Washington, DC that makes the American taxpayer $$$....I think Trump needs to cool it on the overun attacks.

@GoldFinger1969 said:

Since the Fed is the 1 institution in Washington, DC that makes the American taxpayer $$$....I think Trump needs to cool it on the overun attacks.

LOL. The 2008 financial crisis which has required trillions of dollars of bailouts that continue to this day seems a very steep price to pay for those "profits" which are probably entirely fictitious once you inflation-adjust them. And, yes, the Federal Reserve is wholly at fault for the 2008 financial crisis through it's utter failure to regulate the banking system. Former regulator William K. Black (author of The Best to Rob a Bank is to Own a Bank) testified before Congress on this.

@batumi said:

Word is Powell is saying diving boards will be installed on the top floor of his bloated white elephant project.

The architecture of the Mariner Eccles Building is very ornate and requires specialized labor and materials. The cost overruns even BEFORE Covid were going to be there.

Since the Fed is the 1 institution in Washington, DC that makes the American taxpayer $$$....I think Trump needs to cool it on the overun attacks.

I was wondering about that. The Federal Reserve is a private bank. Is there a reason why taxpayers care how much they spend on their buildings? The amount sounds extremely excessive. I'm not familiar with the building but I know you can build a lot for that kind of money.

@batumi said:

Word is Powell is saying diving boards will be installed on the top floor of his bloated white elephant project.

The architecture of the Mariner Eccles Building is very ornate and requires specialized labor and materials. The cost overruns even BEFORE Covid were going to be there.

Since the Fed is the 1 institution in Washington, DC that makes the American taxpayer $$$....I think Trump needs to cool it on the overun attacks.

He wants to control monetary policy in this country. He wants to be the Fed chair.

@MWK said:

And, yes, the Federal Reserve is wholly at fault for the 2008 financial crisis through it's utter failure to regulate the >banking system. Former regulator William K. Black (author of The Best to Rob a Bank is to Own a Bank) testified >before Congress on this.

Congress wrote the rules and the Fed tried to reign in the excesses of the housing and mortgages policies as early as 2002. Congress didn't want to hear about it. I know -- my trade group had a representative from the GSEs bragging about how the Fed was outgunned between HUD, Congress, CRA, etc.

One genius even said during the middle of 2008 as the meltdown was in full-bloom that the government and Fed should "roll the dice" a little.

Black did some good stuff in the 1990's but his predictions and solutions were totally off the wall at times. He was DEAD WRONG on how long the mop-up from 2008-09 GFC would take. And Lehman Brothers problem wasn't so much bad assets as too high leverage.

@ProofCollection said:

I was wondering about that. The Federal Reserve is a private bank. Is there a reason why taxpayers care how much >they spend on their buildings? The amount sounds extremely excessive. I'm not familiar with the building but I know >you can build a lot for that kind of money.

Fed profits are swept to Treasury so in theory there will be a bit less. As FOMC/SOMA operations normalize after the 2022-23 losses, expect the Fed to sweep $50 billion or so annually. So we are talking a 2% hit for a few years.

Numismatist. 54 year member ANA. Former ANA Senior Authenticator. Winner of four ANA Heath Literary Awards; three Wayte and Olga Raymond Literary Awards; Numismatist of the Year Award 2009, and ANA Lifetime Achievement Award 2020. Author of "The Enigmatic Lincoln Cents of 1922," Available now from Whitman or Amazon.

@GoldFinger1969 said:

Congress wrote the rules and the Fed tried to reign in the excesses of the housing and mortgages policies as early as 2002. Congress didn't want to hear about it. I know -- my trade group had a representative from the GSEs bragging about how the Fed was outgunned between HUD, Congress, CRA, etc.

The Federal Reserve and its incompetent and corrupt members have a neverending bag of excuses for their decades of failures. The housing bubble could have easily been shut down by jacking up the Fed Funds Rate and through HOEPA, powers granted by Congress to the Federal Reserve to shut down mortgage fraud.

One genius even said during the middle of 2008 as the meltdown was in full-bloom that the government and Fed should "roll the dice" a little.

"Rolling the dice" (not a real risk at all) would have meant wiping out the shareholders of Goldman Sach, Morgan Stanley, Citigroup (they need a bailout every ten years or so), Bank of America, Wells Fargo, and maybe JPMorgan, replacing the management, making criminal referrals, and recapitalizing the banks by converting some of the bondholders to equity assuming that there is anything there. This is precisely what the Scandinavian countries did in the early 1990s when they had a housing bubble and they recovered very quickly without burdening the entire population with bailing out corrupt management. Also, contrary to the lies told by Paulson, the economy would not have melted down or disintegrated. The banks would still open; the ATMs would still work; people's deposits would still be there. The only real differences are that the management would be changed, fraud would no longer be permitted, and shareholders would be wiped out while bond holders took a haircut or got wiped out depending on how bad the fraud was.

Black did some good stuff in the 1990's but his predictions and solutions were totally off the wall at times. He was DEAD WRONG on how long the mop-up from 2008-09 GFC would take. And Lehman Brothers problem wasn't so much bad assets as too high leverage.

Black's expertise is not in timing things but regulation on which he is a well-known, well-experienced, and well-respected expert. It is impossible for anyone without dictatorial control to predict a priori how long it would take to clean up the 2008 crash given all the interests involved who were more interested in saving their own asses than doing the right thing.

As for Lehman Brothers and all of Wall Street, it was excessive leverage on crappy, fraudulent assets (borrowers not even making the first mortgage payment) that they should have known better than to buy even without any leverage. The assets were garbage, they were fraudulently rated by the ratings agencies, and the only people who truly made money on that junk were the intelligent people and their copy cats who shorted it the correct way.

@GoldFinger1969 said:

Congress wrote the rules and the Fed tried to reign in the excesses of the housing and mortgages policies as early as 2002. Congress didn't want to hear about it. I know -- my trade group had a representative from the GSEs bragging about how the Fed was outgunned between HUD, Congress, CRA, etc.

The Federal Reserve and its incompetent and corrupt members have a neverending bag of excuses for their decades of failures. The housing bubble could have easily been shut down by jacking up the Fed Funds Rate and through HOEPA, powers granted by Congress to the Federal Reserve to shut down mortgage fraud.

didn't read it all.

fed funds rate is an overnight rate. currently, home mortgage rates go off the 10 year bond. they can set the fed funds rate at 5%, but if the bond market think the economy is happily growing such that one day the ffr is 0.25% and the 10yr is 3% then the next the ffr is 5%... the 10yr bond is not going up to 10%. the market sets that and it is based off the economy not the ffr.

also, in some incredibly stupid and probably meant to be opaque reason, the bankers would start putting out crap about libor instead(london interbank offer rate) don't ask me what london has to do with fargo, nd but that's what they did back then. so messing with american rates then would have gone against the bs that they were either selling or mysteriously using.

the real culprit wasn't rates, it was the fraud, sub-prime loans, speculation allowed by banks for people with traditionally way over extended credit. now, the first cracks did come from one foolish action everyone was doing: speculating and trying to buy high then sell higher. eventually new homes were being built faster to the point that new home prices were under existing home prices. eventually home prices began to fall (our 3x value over purch price turned into a 2x). the falling prices put people underwater and ceased the rampant speculation. then the fraud and sub-prime hit. there were foreclosures and prices fell more.

the killer wasn't the ffr. it was the speculation, fraud and sub-prime loans. certainly the speculation would have been curtailed with higher rates, but that is no the overnight rates banks use to lend to each other overnight. it is the long-term bonds like the 10yr and that bond market that sets rates. the economic outlook affects that. no one saw what was coming except the big short.

@MWK said:

The Federal Reserve and its incompetent and corrupt members have a neverending bag of excuses for their >decades of failures. The housing bubble could have easily been shut down by jacking up the Fed Funds Rate and >through HOEPA, powers granted by Congress to the Federal Reserve to shut down mortgage fraud.

So the Fed raises rates on honest borrowers to hammer fraud ? I don't think so.

The Fed doesn't control HUD, CRA, or state laws promoting reckless home ownership. That's NOT the Fed's mandate.

"Rolling the dice" (not a real risk at all) would have meant wiping out the shareholders of Goldman Sach, Morgan >Stanley, Citigroup (they need a bailout every ten years or so), Bank of America, Wells Fargo, and maybe JPMorgan, replacing the management, making criminal referrals, and recapitalizing the banks by converting some of the bondholders to equity assuming that there is anything there.

Except none of those banks were "bankrupt" or needed a bailout. GS and JPM declined TARP $$$ and were forced at gunpoint to accept so as to prevent the other banks from being stigmatized.

As a Goldman bondholder, I watched their equity position by the minute in Fall 2008. It never fell below $48 billion.

...bailing out corrupt management. Also, contrary to the lies told by Paulson, the economy would not have melted >down or disintegrated. The banks would still open; the ATMs would still work; people's deposits would still be there. >The only real differences are that the management would be changed, fraud would no longer be permitted, and >shareholders would be wiped out while bond holders took a haircut or got wiped out depending on how bad the >fraud was.

You don't understand systemic risk. Check out the economic and financial response to the mop-up of Bear Stearns (a speed bump) and Lehman Bros. (a systemic meltdown).

The only losses from TARP were from unions (UAW) and small politically-connected banks, not large Wall Street banks.

Black's expertise is not in timing things but regulation on which he is a well-known, well-experienced, and well->respected expert. It is impossible for anyone without dictatorial control to predict a priori how long it would take to >clean up the 2008 crash given all the interests involved who were more interested in saving their own asses than >doing the right thing.

Bernanke did a good job. Compared to European and Japanese banks, we came through with flying colors when we had our baptism of fire. Japan needed 30 years to recover; Europe almost 15 years. We took 2-3.

As for Lehman Brothers and all of Wall Street, it was excessive leverage on crappy, fraudulent assets (borrowers >not even making the first mortgage payment) that they should have known better than to buy even without any >leverage. The assets were garbage, they were fraudulently rated by the ratings agencies, and the only people who >truly made money on that junk were the intelligent people and their copy cats who shorted it the correct way.

True but even if assets are pristine leverage is the killer. Carlye Capital went down in 2007 investing in AAA-rated U.S. Treasury bonds....because at 30-to-1 leverage, a 3% price drop means your equity is wiped out.

Why does most any importat person affiliated with the fed board of directors or the 12 regional federal reserve banks come from the private banking sector. The fed's first unwritten rule is to protect the banks.

When gold and silver move together, it signals the coming end of fiat money.

@GoldFinger1969 said:

So the Fed raises rates on honest borrowers to hammer fraud ? I don't think so.

No. The Fed raises the short term rates to prevent the idiotic "teaser" rate garbage. Borrowers would still be borrowing at rates that are coupled to the ten-year Treasury bond. Also, the Fed could use HOEPA to prevent the zero down payment, 103% loan-to-value mortgages that were so common during the housing bubble.

The Fed doesn't control HUD, CRA, or state laws promoting reckless home ownership. That's NOT the Fed's mandate.

My point is that the Fed doesn't have to control them. The Fed had tools that can prevent any sorts of actions by those agencies to create a housing bubble. The Fed in actuality really only has two critical jobs: protect the purchasing power of the currency (at which they have failed) and protect the banking system (at which they failed and then "redeemed" themselves by robbing everybody else).

Except none of those banks were "bankrupt" or needed a bailout. GS and JPM declined TARP $$$ and were forced at gunpoint to accept so as to prevent the other banks from being stigmatized.

Then why did GS and MS become bank holding companies? Citigroup ("When the music's playing, you have to get up and dance. We're still dancing."), Bank of America (stupidly bought Merrill Lynch and Countrywide Financial), and Wells Fargo were plain bust. The only bank that might have been good was JPMorgan. BTW, GS, if they did survive, only did so because of the CDS from AIG that were made good by the Fed. AIG was bust and GS should have eaten it due to counterparty risk.

The only losses from TARP were from unions (UAW) and small politically-connected banks, not large Wall Street banks.

Care to explain all the crappy paper issued by the banks that were backed by sub-prime loans and packaged into CDOs and CDO^2s? Those products were created by the big banks so they are directly responsible for those losses. The unions and tiny banks could not have created so much fraudulent paper. It takes truly huge organizations to do it.

Meanwhile, the Fed bought up a lot of flaky assets in its Maiden Lane entities. I'm sure the Fed will now claim that there have been no nominal losses on all the garbage it took onto its balance sheet. All you have to do is massively depreciate the currency and so long as there is some sort of collateral, there is no nominal loss. $1M mortgage on a house that has fallen 50% in price? It is easy to make the mortgage whole by spending trillions of dollars bailing out the system and causing massive inflation. The house will recover to its bubble price since the currency isn't worth anything near as much

Bernanke did a good job. Compared to European and Japanese banks, we came through with flying colors when we had our baptism of fire. Japan needed 30 years to recover; Europe almost 15 years. We took 2-3.

Bernanke did a terrible job and I watched the whole thing unfold from the housing bubble. I was one of many thousands, if not millions, of people who knew there was a housing bubble in the early 2000s unlike the so-called specialists who got caught with their pants down and all said, "Who could have known?" There are far more famous people than me who specialize in this area and they had very harsh words for Bernanke's performance.

Bernanke perhaps could be said to have done a good job in putting out the fire. However, he should have seen there was a fire (I'll give the blame to Greenspan for starting it) and he most certainly didn't do anything to put out the fire until it raged out of control. For a graduate of our country's most elite economics programs and a so-called scholar of the Great Depression, it was a pathetic performance.

Note that I will not comment on this topic anymore as it has strayed too far from the topic of this thread. I was extremely annoyed when it was said that the Federal Reserve turns a profit. It is a nominal profit at best and is likely a loss after adjusting for inflation, especially after its reflationary efforts to paper over the devastating 2008 crash. Meanwhile, the Fed is going to be losing money for a long time (Ben Bernanke himself has said this although he used obfuscatory language) thanks to all the UST bonds on its balance sheet that were purchased when coupons were much, much lower.

@derryb said:

Why does most any importat person affiliated with the fed board of directors or the 12 regional federal reserve >banks come from the private banking sector. The fed's first unwritten rule is to protect the banks.

Why does anybody on a medical or drug review board have a medical degree ? Because we don't want the uninformed deciding things they are unqualified to comment on.

Who do you want on the Fed -- construction workers who barely got through high school ? The homeless ? Bank tellers ?

The genius of the Fed continues to this day as we have the best monetary people in the world.

@derryb said:

Why does most any importat person affiliated with the fed board of directors or the 12 regional federal reserve >banks come from the private banking sector. The fed's first unwritten rule is to protect the banks.

Why does anybody on a medical or drug review board have a medical degree ? Because we don't want the uninformed deciding things they are unqualified to comment on.

Who do you want on the Fed -- construction workers who barely got through high school ? The homeless ? Bank tellers ?

The genius of the Fed continues to this day as we have the best monetary people in the world.

The way things are today, it appears we would have been better off with construction workers,bank tellers and the homeless running things.

@batumi said:

The way things are today, it appears we would have been better off with construction workers,bank tellers and the >homeless running things.

We have the best Central Bankers on the globe. We forget that as we take them for granted.

I've studied central bankers for 5 decades. Unless you want to bring up Paul Volcker and Karl Otto Poehl, it's tough to beat our successors since then (except Janet Yellen, who I thought was a lightweight).

@derryb said:

Why does most any importat person affiliated with the fed board of directors or the 12 regional federal reserve >banks come from the private banking sector. The fed's first unwritten rule is to protect the banks.

Why does anybody on a medical or drug review board have a medical degree ? Because we don't want the uninformed deciding things they are unqualified to comment on.

Who do you want on the Fed -- construction workers who barely got through high school ? The homeless ? Bank tellers ?

The genius of the Fed continues to this day as we have the best monetary people in the world.

@batumi said:

The way things are today, it appears we would have been better off with construction workers,bank tellers and the >homeless running things.

We have the best Central Bankers on the globe. We forget that as we take them for granted.

I've studied central bankers for 5 decades. Unless you want to bring up Paul Volcker and Karl Otto Poehl, it's tough to beat our successors since then (except Janet Yellen, who I thought was a lightweight).

It's hard to think of them in these terms. They are all pin striped bandits.

Numismatist. 54 year member ANA. Former ANA Senior Authenticator. Winner of four ANA Heath Literary Awards; three Wayte and Olga Raymond Literary Awards; Numismatist of the Year Award 2009, and ANA Lifetime Achievement Award 2020. Author of "The Enigmatic Lincoln Cents of 1922," Available now from Whitman or Amazon.

@Bayard1908 said:

I should be thankful for parasites and their self dealing system? No thanks.

If you prefer another CB by all means let us know.

If you really knew about self-dealing and parasites, you'd be railing about certain politicians and the GSEs and NGOs who sponge off the private sector.

@Bayard1908 said:

I should be thankful for parasites and their self dealing system? No thanks.

If you prefer another CB by all means let us know.

If you really knew about self-dealing and parasites, you'd be railing about certain politicians and the GSEs and NGOs who sponge off the private sector.

I'd prefer not to have a CB. We don't need one. The debt money system is a scam.

Comments

Are we having fun yet?

Such as.....?")

Maybe in the 1970's for a few years, when currencies went from fixed to floating and inflation roared.

Your statement about "Western bankers" is patently untrue since governments have been the instigators, even subtly coercing "Western bankers" into buying government debt (i.e., Europe).

My experience in the few times I stopped by the metals trading desk -- I spent much more time at the bond desk -- is that contango was a real headwing for futures trading given the negative carry. This problem was exaccerbated with leverage which many hedge funds and institutions utilized.

Never understood these wide-spreads when the price rises or volumes pick up. That's a really wide spread when it should have narrowed, IMO.

Scotsman is paying just under spot, selling for about spot + $150.

I knew it would happen.

https://scoins.com/pricelist/tradingsheet.aspx

I knew it would happen.

Platinum has always had pretty wide spreads. It's a low volume metal. I'm guessing most dealers have to pay less and charge more because there really isn't a ton of retail demand. It's even worse for metals like Rhodium.

Word is Powell is saying diving boards will be installed on the top floor of his bloated white elephant project.

The architecture of the Mariner Eccles Building is very ornate and requires specialized labor and materials. The cost overruns even BEFORE Covid were going to be there.

Since the Fed is the 1 institution in Washington, DC that makes the American taxpayer $$$....I think Trump needs to cool it on the overun attacks.

LOL. The 2008 financial crisis which has required trillions of dollars of bailouts that continue to this day seems a very steep price to pay for those "profits" which are probably entirely fictitious once you inflation-adjust them. And, yes, the Federal Reserve is wholly at fault for the 2008 financial crisis through it's utter failure to regulate the banking system. Former regulator William K. Black (author of The Best to Rob a Bank is to Own a Bank) testified before Congress on this.

I was wondering about that. The Federal Reserve is a private bank. Is there a reason why taxpayers care how much they spend on their buildings? The amount sounds extremely excessive. I'm not familiar with the building but I know you can build a lot for that kind of money.

He wants to control monetary policy in this country. He wants to be the Fed chair.

Knowledge is the enemy of fear

Congress wrote the rules and the Fed tried to reign in the excesses of the housing and mortgages policies as early as 2002. Congress didn't want to hear about it. I know -- my trade group had a representative from the GSEs bragging about how the Fed was outgunned between HUD, Congress, CRA, etc.

One genius even said during the middle of 2008 as the meltdown was in full-bloom that the government and Fed should "roll the dice" a little.")

Black did some good stuff in the 1990's but his predictions and solutions were totally off the wall at times. He was DEAD WRONG on how long the mop-up from 2008-09 GFC would take. And Lehman Brothers problem wasn't so much bad assets as too high leverage.

Fed profits are swept to Treasury so in theory there will be a bit less. As FOMC/SOMA operations normalize after the 2022-23 losses, expect the Fed to sweep $50 billion or so annually. So we are talking a 2% hit for a few years.

Gold and Silver ripping higher tonight. Might get $4700 and $94 soon.

Successful BST with drddm, BustDMs, Pnies20, lkeigwin, pursuitofliberty, Bullsitter, felinfoel, SPalladino

$5 Type Set https://www.pcgs.com/setregistry/u-s-coins/type-sets/half-eagle-type-set-circulation-strikes-1795-1929/album/344192

CBH Set https://www.pcgs.com/setregistry/everyman-collections/everyman-half-dollars/everyman-capped-bust-half-dollars-1807-1839/album/345572

“And they’re off….”

The Federal Reserve and its incompetent and corrupt members have a neverending bag of excuses for their decades of failures. The housing bubble could have easily been shut down by jacking up the Fed Funds Rate and through HOEPA, powers granted by Congress to the Federal Reserve to shut down mortgage fraud.

"Rolling the dice" (not a real risk at all) would have meant wiping out the shareholders of Goldman Sach, Morgan Stanley, Citigroup (they need a bailout every ten years or so), Bank of America, Wells Fargo, and maybe JPMorgan, replacing the management, making criminal referrals, and recapitalizing the banks by converting some of the bondholders to equity assuming that there is anything there. This is precisely what the Scandinavian countries did in the early 1990s when they had a housing bubble and they recovered very quickly without burdening the entire population with bailing out corrupt management. Also, contrary to the lies told by Paulson, the economy would not have melted down or disintegrated. The banks would still open; the ATMs would still work; people's deposits would still be there. The only real differences are that the management would be changed, fraud would no longer be permitted, and shareholders would be wiped out while bond holders took a haircut or got wiped out depending on how bad the fraud was.

Black's expertise is not in timing things but regulation on which he is a well-known, well-experienced, and well-respected expert. It is impossible for anyone without dictatorial control to predict a priori how long it would take to clean up the 2008 crash given all the interests involved who were more interested in saving their own asses than doing the right thing.

As for Lehman Brothers and all of Wall Street, it was excessive leverage on crappy, fraudulent assets (borrowers not even making the first mortgage payment) that they should have known better than to buy even without any leverage. The assets were garbage, they were fraudulently rated by the ratings agencies, and the only people who truly made money on that junk were the intelligent people and their copy cats who shorted it the correct way.

didn't read it all.

fed funds rate is an overnight rate. currently, home mortgage rates go off the 10 year bond. they can set the fed funds rate at 5%, but if the bond market think the economy is happily growing such that one day the ffr is 0.25% and the 10yr is 3% then the next the ffr is 5%... the 10yr bond is not going up to 10%. the market sets that and it is based off the economy not the ffr.

also, in some incredibly stupid and probably meant to be opaque reason, the bankers would start putting out crap about libor instead(london interbank offer rate) don't ask me what london has to do with fargo, nd but that's what they did back then. so messing with american rates then would have gone against the bs that they were either selling or mysteriously using.

the real culprit wasn't rates, it was the fraud, sub-prime loans, speculation allowed by banks for people with traditionally way over extended credit. now, the first cracks did come from one foolish action everyone was doing: speculating and trying to buy high then sell higher. eventually new homes were being built faster to the point that new home prices were under existing home prices. eventually home prices began to fall (our 3x value over purch price turned into a 2x). the falling prices put people underwater and ceased the rampant speculation. then the fraud and sub-prime hit. there were foreclosures and prices fell more.

the killer wasn't the ffr. it was the speculation, fraud and sub-prime loans. certainly the speculation would have been curtailed with higher rates, but that is no the overnight rates banks use to lend to each other overnight. it is the long-term bonds like the 10yr and that bond market that sets rates. the economic outlook affects that. no one saw what was coming except the big short.

So the Fed raises rates on honest borrowers to hammer fraud ? I don't think so.")

The Fed doesn't control HUD, CRA, or state laws promoting reckless home ownership. That's NOT the Fed's mandate.

Except none of those banks were "bankrupt" or needed a bailout. GS and JPM declined TARP $$$ and were forced at gunpoint to accept so as to prevent the other banks from being stigmatized.

As a Goldman bondholder, I watched their equity position by the minute in Fall 2008. It never fell below $48 billion.

You don't understand systemic risk. Check out the economic and financial response to the mop-up of Bear Stearns (a speed bump) and Lehman Bros. (a systemic meltdown).

The only losses from TARP were from unions (UAW) and small politically-connected banks, not large Wall Street banks.

Bernanke did a good job. Compared to European and Japanese banks, we came through with flying colors when we had our baptism of fire. Japan needed 30 years to recover; Europe almost 15 years. We took 2-3.

True but even if assets are pristine leverage is the killer. Carlye Capital went down in 2007 investing in AAA-rated U.S. Treasury bonds....because at 30-to-1 leverage, a 3% price drop means your equity is wiped out.

the banks own the fed, literally

When gold and silver move together, it signals the coming end of fiat money.

ZZzzzzzzzzzz.........ZZZZZzzzzzzzz........")

Why does most any importat person affiliated with the fed board of directors or the 12 regional federal reserve banks come from the private banking sector. The fed's first unwritten rule is to protect the banks.

When gold and silver move together, it signals the coming end of fiat money.

No. The Fed raises the short term rates to prevent the idiotic "teaser" rate garbage. Borrowers would still be borrowing at rates that are coupled to the ten-year Treasury bond. Also, the Fed could use HOEPA to prevent the zero down payment, 103% loan-to-value mortgages that were so common during the housing bubble.

My point is that the Fed doesn't have to control them. The Fed had tools that can prevent any sorts of actions by those agencies to create a housing bubble. The Fed in actuality really only has two critical jobs: protect the purchasing power of the currency (at which they have failed) and protect the banking system (at which they failed and then "redeemed" themselves by robbing everybody else).

Then why did GS and MS become bank holding companies? Citigroup ("When the music's playing, you have to get up and dance. We're still dancing."), Bank of America (stupidly bought Merrill Lynch and Countrywide Financial), and Wells Fargo were plain bust. The only bank that might have been good was JPMorgan. BTW, GS, if they did survive, only did so because of the CDS from AIG that were made good by the Fed. AIG was bust and GS should have eaten it due to counterparty risk.

Care to explain all the crappy paper issued by the banks that were backed by sub-prime loans and packaged into CDOs and CDO^2s? Those products were created by the big banks so they are directly responsible for those losses. The unions and tiny banks could not have created so much fraudulent paper. It takes truly huge organizations to do it.

Meanwhile, the Fed bought up a lot of flaky assets in its Maiden Lane entities. I'm sure the Fed will now claim that there have been no nominal losses on all the garbage it took onto its balance sheet. All you have to do is massively depreciate the currency and so long as there is some sort of collateral, there is no nominal loss. $1M mortgage on a house that has fallen 50% in price? It is easy to make the mortgage whole by spending trillions of dollars bailing out the system and causing massive inflation. The house will recover to its bubble price since the currency isn't worth anything near as much

Bernanke did a terrible job and I watched the whole thing unfold from the housing bubble. I was one of many thousands, if not millions, of people who knew there was a housing bubble in the early 2000s unlike the so-called specialists who got caught with their pants down and all said, "Who could have known?" There are far more famous people than me who specialize in this area and they had very harsh words for Bernanke's performance.

Bernanke perhaps could be said to have done a good job in putting out the fire. However, he should have seen there was a fire (I'll give the blame to Greenspan for starting it) and he most certainly didn't do anything to put out the fire until it raged out of control. For a graduate of our country's most elite economics programs and a so-called scholar of the Great Depression, it was a pathetic performance.

Note that I will not comment on this topic anymore as it has strayed too far from the topic of this thread. I was extremely annoyed when it was said that the Federal Reserve turns a profit. It is a nominal profit at best and is likely a loss after adjusting for inflation, especially after its reflationary efforts to paper over the devastating 2008 crash. Meanwhile, the Fed is going to be losing money for a long time (Ben Bernanke himself has said this although he used obfuscatory language) thanks to all the UST bonds on its balance sheet that were purchased when coupons were much, much lower.

.

That is not a convincing rebuttal.

In fact, it appears to be an acknowledgement that the "FED" IS owned by the member banks.

.

Why does anybody on a medical or drug review board have a medical degree ? Because we don't want the uninformed deciding things they are unqualified to comment on.

Who do you want on the Fed -- construction workers who barely got through high school ? The homeless ? Bank tellers ?

The genius of the Fed continues to this day as we have the best monetary people in the world.

futures hit 4700

kitco session high - 4695

and just like that kitco 4700

Yeah, all of the markets are generally within $20 of each other, I'm not sure anyone cares about the tiny variances.

And then $4725+

Successful BST with drddm, BustDMs, Pnies20, lkeigwin, pursuitofliberty, Bullsitter, felinfoel, SPalladino

$5 Type Set https://www.pcgs.com/setregistry/u-s-coins/type-sets/half-eagle-type-set-circulation-strikes-1795-1929/album/344192

CBH Set https://www.pcgs.com/setregistry/everyman-collections/everyman-half-dollars/everyman-capped-bust-half-dollars-1807-1839/album/345572

OK, I'm behind the ball today, computer problems. Gold at $2800+. I'm seeing a new ATH around $4847. Wow!

Come on $5000.

Successful BST with drddm, BustDMs, Pnies20, lkeigwin, pursuitofliberty, Bullsitter, felinfoel, SPalladino

$5 Type Set https://www.pcgs.com/setregistry/u-s-coins/type-sets/half-eagle-type-set-circulation-strikes-1795-1929/album/344192

CBH Set https://www.pcgs.com/setregistry/everyman-collections/everyman-half-dollars/everyman-capped-bust-half-dollars-1807-1839/album/345572

The way things are today, it appears we would have been better off with construction workers,bank tellers and the homeless running things.

We have the best Central Bankers on the globe. We forget that as we take them for granted.

I've studied central bankers for 5 decades. Unless you want to bring up Paul Volcker and Karl Otto Poehl, it's tough to beat our successors since then (except Janet Yellen, who I thought was a lightweight).

Turned profitable in 2026 (final figures coming out soon) and should earn about $100-$125 billion per year through 2035.")

.

The only "genius" in the FED is "evil".

.

It's hard to think of them in these terms. They are all pin striped bandits.

Gold over $4900 now.

As of a few minutes ago

Exciting times.

Successful BST with drddm, BustDMs, Pnies20, lkeigwin, pursuitofliberty, Bullsitter, felinfoel, SPalladino

$5 Type Set https://www.pcgs.com/setregistry/u-s-coins/type-sets/half-eagle-type-set-circulation-strikes-1795-1929/album/344192

CBH Set https://www.pcgs.com/setregistry/everyman-collections/everyman-half-dollars/everyman-capped-bust-half-dollars-1807-1839/album/345572

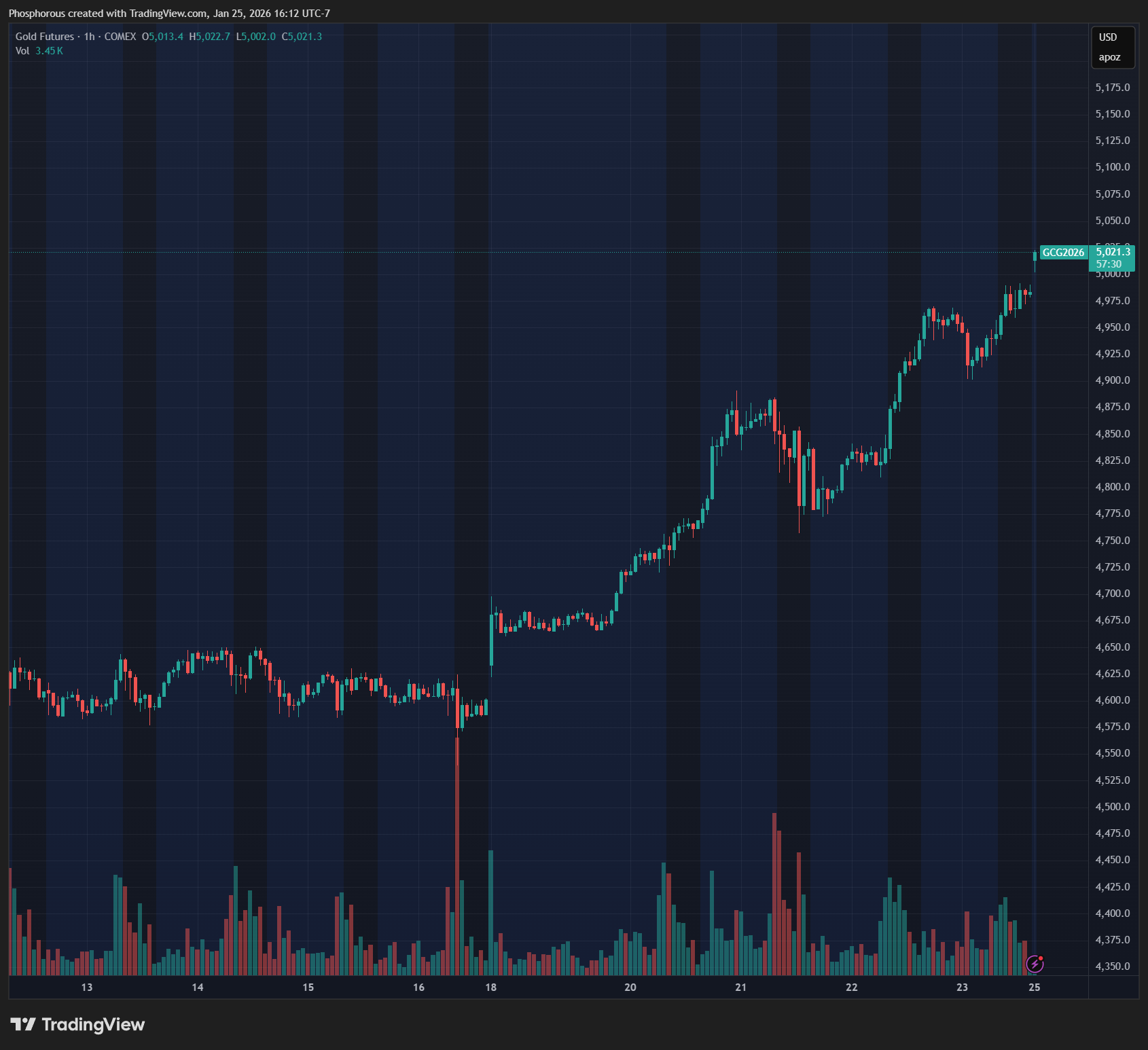

$5000 is here! $5023.4 at the moment.

good time to own a pawn shop

More new highs! Get ready to be rich!

Congratulations to ProofCollection for updating the Title with higher targets the last year or so !!!")

5110.90 kitco! now 5107.90 ath on futures.

spot demand is strong.

I should be thankful for parasites and their self dealing system? No thanks.

Charts just before Midnight my time

Are you going to retire now?

Congrats to all those that ignored the forum naysayers and bought gold and silver at FUN.

Successful BST with drddm, BustDMs, Pnies20, lkeigwin, pursuitofliberty, Bullsitter, felinfoel, SPalladino

$5 Type Set https://www.pcgs.com/setregistry/u-s-coins/type-sets/half-eagle-type-set-circulation-strikes-1795-1929/album/344192

CBH Set https://www.pcgs.com/setregistry/everyman-collections/everyman-half-dollars/everyman-capped-bust-half-dollars-1807-1839/album/345572

If you prefer another CB by all means let us know.

If you really knew about self-dealing and parasites, you'd be railing about certain politicians and the GSEs and NGOs who sponge off the private sector.

I'd prefer not to have a CB. We don't need one. The debt money system is a scam.